Trump’s Current Presidency and the Crisis of Post–World War II Globalization

I. Executive Judgment

Donald Trump’s current presidency should be assessed as a live stress event in the crisis of post–World War II globalization. The subject is not Trump in isolation. The subject is the U.S.-led globalization model that emerged after 1945, expanded through the Cold War and post-Cold War eras, and now faces structural stress across trade, monetary policy, alliances, industrial capacity, energy, borders, digital finance, and domestic legitimacy.

Trump’s first term exposed the instability of that model. His current presidency is testing whether disruption can be converted into doctrine. The relevant question is not whether Trump personally designed the transition toward multipolarity. He did not. The more consequential question is whether the United States can manage the transition from a dollar-centered, security-backed, China-integrated, finance-heavy, supply-chain-dependent globalization model toward a more resilient economic-security order without triggering trade escalation, alliance fracture, monetary instability, authoritarian drift, or domestic breakdown.

The current policy environment makes this more than a retrospective question. The January 2025 America First Trade Policy memorandum directed federal agencies to review trade deficits, unfair practices, de minimis import rules, tariff revenue, export controls, China-related economic exposure, and the economic and national-security implications of trade policy. USTR’s 2025 trade agenda links trade policy to increasing manufacturing’s share of GDP, increasing real median household income, and reducing the goods trade deficit. NATO’s 2025 Hague commitment sets a target of investing 5 percent of GDP annually in core defense and defense/security-related spending by 2035, including at least 3.5 percent for core defense requirements.

Strategic judgment: Trump is not the architect of multipolarity. He is the political figure through whom the United States is actively renegotiating the terms of the post–World War II globalization order it once managed.

II. Definition: Post–World War II Globalization

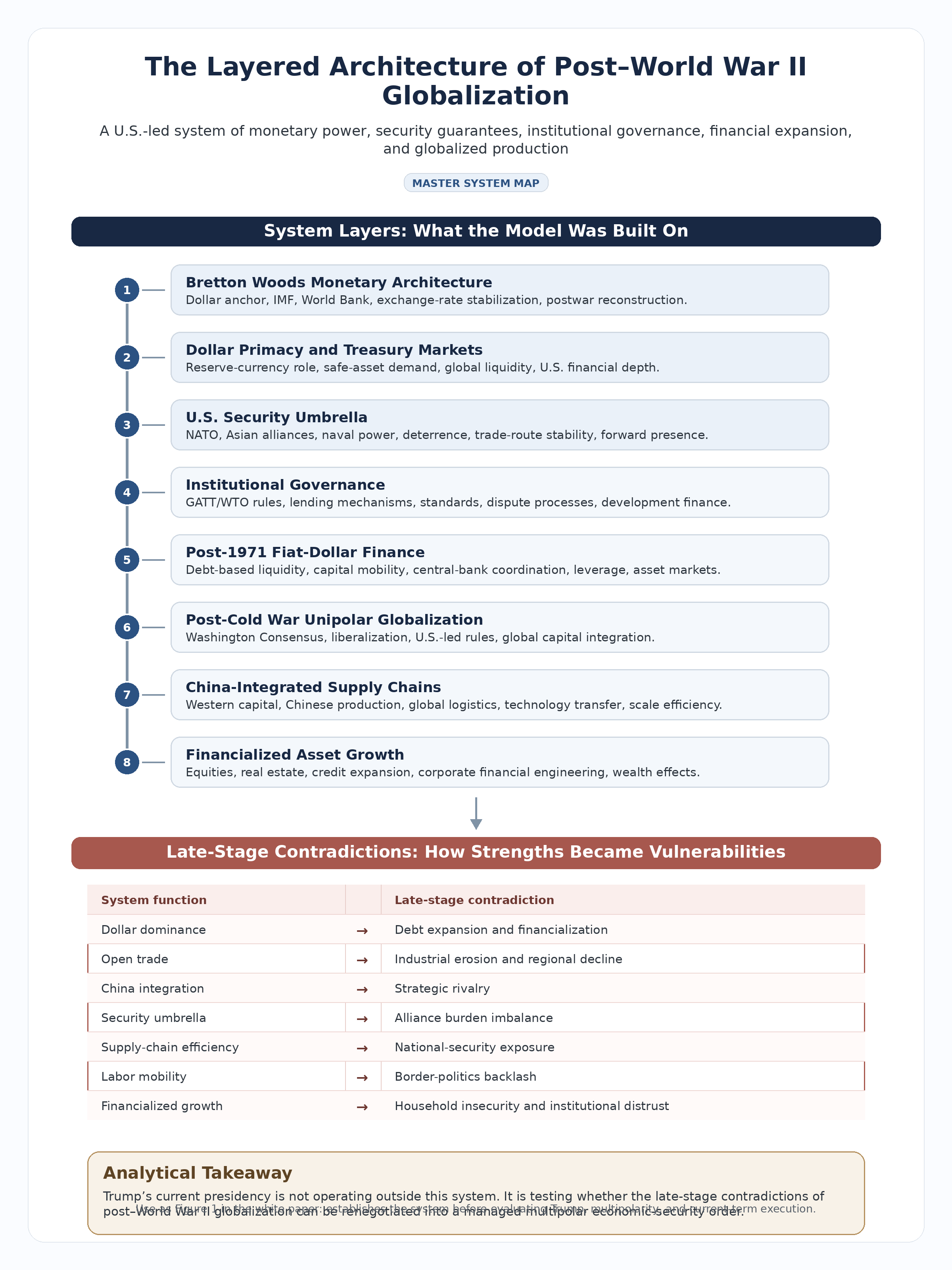

For purposes of this analysis, post–World War II globalization refers to the layered U.S.-led system that combined Bretton Woods monetary institutions, Cold War security guarantees, post-1971 dollar-financial dominance, post-Cold War unipolarity, WTO-era trade liberalization, China-integrated supply chains, and financialized asset growth.

This was not a single static order. It evolved through several phases.

The first was the Bretton Woods phase, in which the United States anchored postwar monetary reconstruction through the dollar, the IMF, the World Bank, and exchange-rate stabilization. The dollar’s centrality made U.S. monetary credibility a global public good.

The second was the Cold War security-globalization phase, in which U.S. military alliances, open Western markets, development finance, trade expansion, and dollar liquidity supported a U.S.-led capitalist bloc. Economic globalization and security strategy were inseparable: the United States supplied not only markets and liquidity, but also protection.

The third was the post-1971 fiat-dollar phase, in which the dollar remained the central global currency after formal gold convertibility ended. This made the system more flexible, but also more dependent on U.S. Treasury markets, debt-based liquidity, financial depth, central-bank coordination, and confidence in American institutions.

The fourth was the post-Cold War unipolar phase, in which the Soviet collapse, WTO expansion, China’s integration into global markets, offshored production, financial liberalization, technological integration, and global supply chains produced the high point of U.S.-led globalization.

This model produced major gains: reconstruction, trade growth, lower consumer costs, technological diffusion, financial liquidity, allied stability, and U.S. geopolitical influence. It also accumulated structural costs: industrial offshoring, debt expansion, financialization, regional inequality, trade imbalances, supply-chain fragility, reserve-currency burdens, China dependence, and declining trust among domestic constituencies that experienced globalization as loss rather than security.

Trump’s presidency should therefore be assessed not against “globalization” in the abstract, but against this specific historical model: post–World War II globalization as organized around U.S. monetary power, U.S. security guarantees, open trade, financial integration, China-linked supply chains, and post-Cold War unipolarity.

III. Basis of Analysis

This memorandum condenses a 21-section white paper developed from a broader analytical review of post–World War II globalization, Trump-era policy, and the transition from U.S.-led unipolarity toward multipolar competition. The underlying work examines Bretton Woods, the post-1971 dollar system, China’s rise, Section 301 tariffs, NATO burden-sharing, de-dollarization pressures, industrial policy, supply-chain resilience, energy and commodities, immigration and labor markets, financialization, COVID-era emergency governance, and the risks of bloc formation, digital surveillance infrastructure, and great-power rivalry.

The evidentiary base relies primarily on official and institutional sources: Federal Reserve research on dollar primacy, IMF reserve-currency and geoeconomic-fragmentation data, USTR trade-policy documents, CBO long-term fiscal projections, CRS reporting, NATO defense-spending materials, BIS analysis of digital money, IEA energy-security analysis, Treasury materials, and U.S. national-security documents.

Several current metrics frame the analysis. The Federal Reserve’s 2025 assessment reports that the dollar comprised 58 percent of disclosed global official foreign reserves in 2024, down from a peak of 72 percent in 2001, while remaining far ahead of the euro and renminbi. USTR’s 2026 trade-policy materials report that the U.S. goods trade deficit reached $1.24 trillion in 2025, while the services surplus rose to $339.5 billion. NATO states that allies committed at the 2025 Hague Summit to invest 5 percent of GDP annually in core defense and defense/security-related spending by 2035, including at least 3.5 percent for core defense requirements.

Interpretive frameworks, including Catherine Austin Fitts-style arguments about financial centralization, digital money, asset control, and public-private governance, are used as analytical lenses rather than as standalone evidence. They are useful for asking whether multipolarity decentralizes power or merely reorganizes control across competing blocs, but contested claims within that framework require independent corroboration.

IV. Analytical Caution

This memorandum does not argue that Trump personally designed the transition to multipolarity. It does not assume that every Trump policy is strategically coherent. It does not claim that tariffs automatically restore industrial capacity, that alliance pressure automatically improves security, or that disruption itself is evidence of strategy.

It also does not assume that post–World War II globalization was simply a failure. The system generated reconstruction, trade expansion, financial liquidity, technological diffusion, allied stability, and decades of American influence. Its achievements were real.

The argument is narrower and stronger: the system’s late-stage contradictions have become too large to manage through the assumptions of the post-Cold War consensus. Trump’s presidency matters because it forces those contradictions into open political and policy conflict. His first term revealed the instability of the model. His current presidency is testing whether that instability can be converted into a durable operating doctrine.

This distinction is essential. A serious analysis must avoid both anti-Trump reductionism and pro-Trump romanticism. Trump is neither an accidental aberration nor a flawless strategist. He is a volatile transitional figure operating inside a system whose underlying assumptions are failing.

V. Causal Chain

The argument proceeds through a five-step causal sequence.

First, the post–World War II globalization model produced stability and growth while creating structural dependencies. The United States supplied the reserve currency, security guarantees, market access, liquidity, and institutional leadership. This made the United States the operating center of the system, but also created dependence on U.S. debt markets, U.S. military commitments, open trade, and increasingly globalized supply chains.

Second, the post-Cold War expansion of this model intensified its contradictions. The Soviet collapse, WTO expansion, China’s market integration, global supply-chain optimization, and financial liberalization produced efficiency and growth, but also accelerated industrial offshoring, debt expansion, financialization, regional inequality, and strategic dependence on foreign production.

Third, those contradictions weakened domestic legitimacy and strategic resilience. The 2008 financial crisis damaged confidence in Western financial stewardship. China’s rise challenged the engagement consensus. Supply-chain shocks exposed fragility. Border and migration pressures became proxies for state capacity. Asset-market gains increasingly diverged from the lived experience of many workers and communities.

Fourth, Trump’s first term converted latent structural pressure into open political rupture. Trade orthodoxy, China engagement, alliance automaticity, border assumptions, energy constraints, and technocratic multilateralism were all challenged directly.

Fifth, Trump’s current presidency is testing whether rupture can become doctrine. Current policy is attempting to reprice trade, alliances, industrial policy, border control, energy security, and monetary strategy under multipolar conditions. The unresolved question is whether this becomes disciplined transition or unmanaged fragmentation.

VI. Decision Frame

The central question is not whether Trump is personally right or wrong. That framing is too narrow for a serious assessment of the current presidency. The more consequential question is whether the United States can adapt to a world in which the assumptions of post–World War II globalization no longer hold.

That system required the United States to perform several roles simultaneously: reserve-currency issuer, consumer of last resort, alliance guarantor, liquidity provider, military stabilizer, institutional sponsor, and open-market anchor. It was sustainable while the United States retained overwhelming industrial strength, broad domestic consent, unrivaled financial centrality, and a favorable distribution of global power. Those conditions have changed.

The United States remains extraordinarily powerful, but its position is more constrained. China has become a rival industrial and technological pole. Europe is under pressure to assume greater defense and energy responsibility. The dollar remains central, but reserve diversification, sanctions risk, and alternative payment systems are creating pressure at the margins. Supply chains remain global, but they are increasingly judged by resilience and political reliability rather than efficiency alone. Domestic legitimacy is no longer guaranteed.

The decision frame is therefore this:

Can the United States move from financialized, dollar-centered postwar globalization toward productive, sovereign, and alliance-based resilience without triggering systemic instability?

The old model cannot simply be restored. But the transition cannot be allowed to proceed through improvisation alone.

VII. Current Strategic Context

Trump is governing in a more advanced phase of the multipolar transition than during his first term.

During the first term, the central issue was recognition. Trump identified vulnerabilities that the post-Cold War consensus had minimized: China dependence, industrial erosion, trade deficits, allied free-riding, border disorder, and the social costs of financialized globalization. His methods were often blunt and destabilizing, but the issues he elevated proved durable.

In the current presidency, the central issue is execution. The administration is attempting to convert first-term disruption into an operating doctrine. The January 2025 America First Trade Policy memorandum directed federal agencies to review trade deficits, unfair trade practices, tariff revenue, de minimis import rules, export controls, China-related economic exposure, and trade tools linked to economic and national security. USTR’s 2025 trade agenda states that trade policy should be coordinated to increase manufacturing’s share of GDP, increase real median household income, and reduce the goods trade deficit.

The administration’s reciprocal-tariff framework also treats persistent goods trade deficits as an economic and national-security problem, stating that the January 2025 memorandum directed investigation of the causes and risks of large and persistent annual goods deficits.

The alliance environment has also moved from rhetorical pressure to institutional adjustment. NATO’s Hague commitment establishes a 5 percent GDP defense-investment target by 2035, including 3.5 percent for core defense requirements. This does not eliminate alliance tension. It raises the stakes. If allies meet the target, the U.S. security umbrella becomes more sustainable. If they do not, U.S. frustration with allied dependence will intensify.

The current environment is therefore no longer defined by whether post-WWII globalization is under strain. That is established. The live question is whether the United States can manage the transition from a dollar-centered, U.S.-secured, China-integrated, finance-heavy, supply-chain-dependent model into a more resilient multipolar economic-security architecture.

VIII. Core Thesis

Donald Trump’s presidency should be understood as a two-phase stress event in the crisis of post–World War II globalization. His first term exposed the instability of the U.S.-led model that combined dollar dominance, alliance guarantees, open trade, China-integrated supply chains, financialization, and post-Cold War unipolarity. His current presidency is testing whether that exposure can be converted into an operating doctrine for multipolar competition.

The central issue is not whether Trump created the transition. He did not. The central issue is whether the United States can manage the transition from late-stage postwar globalization toward a more resilient, productive, and constitutionally accountable economic-security order.

This transition is driven by seven pressures.

First, the model struggles to reconcile dollar dominance with debt expansion. The United States benefits from issuing the dominant reserve currency, but that role depends on deep debt markets, fiscal credibility, and global trust.

Second, it struggles to reconcile globalization with industrial decline. The post-Cold War model lowered costs and expanded corporate margins, but weakened domestic production in strategically important sectors.

Third, it struggles to reconcile China engagement with strategic competition. The assumption that integration would make China more liberal, cooperative, and compatible with U.S.-led rules has failed as a governing premise.

Fourth, it struggles to reconcile alliance leadership with fiscal and political fatigue. The United States still benefits from alliances, but domestic tolerance for underpriced security guarantees has weakened.

Fifth, it struggles to reconcile open supply chains with national-security vulnerability. Efficiency-centered globalization created dependencies in semiconductors, pharmaceuticals, critical minerals, energy systems, shipping, telecommunications, and defense inputs.

Sixth, it struggles to reconcile immigration and labor mobility with domestic legitimacy. Border policy has become a proxy for state capacity, labor-market pressure, public finance, sovereignty, and political trust.

Seventh, it struggles to reconcile financialized growth with broad-based economic security. Asset inflation can support household wealth and institutional balance sheets, but it cannot substitute for rising real wages, regional renewal, affordable housing, and productive investment.

Trump’s diagnosis is often closer to structural reality than his critics admit. His execution remains more uncertain, volatile, and institutionally risky than his supporters claim.

IX. Phase I: First-Term Rupture

Trump’s first term broke the post-Cold War consensus but did not replace it with a complete new model.

His trade policy challenged the assumption that free trade automatically served U.S. national interests. The Section 301 tariffs on China were blunt and costly, but they forced policymakers to reconsider trade as a matter of industrial capacity and national security rather than consumer-price efficiency alone.

His China policy challenged the assumption that engagement would produce convergence. China was no longer treated merely as a trading partner or manufacturing platform. It was increasingly treated as a strategic competitor whose industrial policy, technology ambitions, military modernization, and state-capitalist model altered the logic of globalization.

His alliance policy challenged automaticity. NATO pressure was disruptive, but it addressed a real structural question: how long could the United States maintain global security guarantees while facing fiscal pressure, industrial weakness, and intensifying competition with China?

His border policy challenged the political sustainability of open-ended globalization. Immigration became linked to sovereignty, wages, welfare-state capacity, social trust, and state enforcement credibility.

His energy policy challenged the idea that energy production was secondary to climate diplomacy or market allocation. It treated energy abundance as an instrument of national autonomy.

The limitation of the first term was execution. The administration often identified real vulnerabilities but lacked the institutional discipline to convert diagnosis into durable strategy. Tariffs did not automatically rebuild industry. Alliance pressure sometimes weakened trust. China policy alternated between structural confrontation and transactional bargaining. Fiscal policy did not resolve the debt problem. Financial markets remained central to the administration’s measure of economic success.

The first term’s importance is therefore not that it solved the crisis of post-WWII globalization. It made the crisis impossible to ignore.

X. Phase II: Current-Term Execution

The current presidency is testing whether rupture can become doctrine.

The administration’s current trade architecture is more explicit than in the first term. The America First Trade Policy memorandum directs agencies to review unfair trade practices, tariff revenues, counterfeit goods, fentanyl-related risks, export controls, China exposure, and strategic technology leakage. USTR’s 2025 agenda links trade policy to manufacturing’s share of GDP, real median household income, and the reduction of the goods trade deficit. USTR’s 2026 trade-policy agenda reports that the U.S. goods deficit reached $1.24 trillion in 2025, indicating that trade imbalance remains a central policy concern.

The current alliance architecture is also more developed. NATO’s 5 percent commitment transforms burden-sharing from a rhetorical demand into an institutional benchmark. This does not mean the alliance problem is solved. It means the problem has moved from diplomatic complaint to implementation: procurement, industrial capacity, infrastructure resilience, defense production, cyber readiness, and political willingness.

The current monetary environment is more complicated than in the first term. The dollar remains dominant, but its margin of uncontested authority is narrowing. The Federal Reserve reports that the dollar comprised 58 percent of disclosed global official reserves in 2024, down from 72 percent in 2001. This supports a nuanced conclusion: the dollar is not collapsing, but the system is diversifying at the margins.

The current industrial environment is more strategic. Semiconductors, defense production, critical minerals, ports, shipbuilding, pharmaceuticals, grid infrastructure, artificial intelligence systems, and telecommunications are no longer treated as ordinary market sectors. They are now part of the security architecture.

The current presidency is therefore operating on the premise that trade is security, production is sovereignty, energy is autonomy, borders are state capacity, alliances require burden-sharing, and monetary power depends on domestic strength.

That premise is coherent. Whether implementation is coherent remains the open question.

XI. The Strategic Test of the Current Presidency

The current presidency is testing six propositions.

1. Can tariffs rebuild capacity rather than merely raise costs?

Tariffs may create leverage, protect selected sectors, and expose dependency. But they do not automatically build factories, train workers, expand ports, secure minerals, or create technological leadership. Their success depends on whether they are paired with permitting reform, workforce development, tax incentives, procurement strategy, energy reliability, infrastructure investment, and allied supply-chain coordination.

2. Can the United States compete with China without isolating itself?

China competition is unavoidable if China remains a rival industrial and technological pole. But unilateral escalation can isolate the United States from allies whose cooperation is necessary for export controls, investment screening, technology standards, maritime security, and supply-chain diversification. The strategic task is to make China competition coalition-based rather than merely bilateral.

3. Can NATO burden-sharing increase without weakening alliance trust?

Higher allied defense spending is structurally necessary. But alliances are not protection rackets. They are strategic assets that provide bases, intelligence, interoperability, legitimacy, and regional reach. The 5 percent benchmark strengthens the burden-sharing argument, but implementation must preserve alliance cohesion.

4. Can dollar credibility be preserved under fiscal strain?

The dollar remains the central currency of global finance, but dominance depends on trust, liquidity, fiscal seriousness, rule of law, and institutional credibility. The Federal Reserve data show continued reserve dominance, but also a long-term decline in reserve share from its 2001 peak.

5. Can border enforcement restore legitimacy while preserving lawful economic function?

Border control is now a core state-capacity issue. But a credible strategy must distinguish unlawful entry, asylum administration, temporary labor needs, high-skill immigration, humanitarian obligations, employer enforcement, and domestic wage protection. Enforcement without labor-market strategy is incomplete. Immigration without state control is politically destabilizing.

6. Can digital financial modernization avoid becoming control infrastructure?

Digital money, instant payments, sanctions compliance, identity systems, and financial surveillance can improve efficiency and security. They can also enable conditional access, politicized exclusion, and administrative overreach. A rigorous analysis should avoid conspiratorial claims while recognizing the real governance stakes of programmable and highly monitored financial systems.

XII. Core Findings

Finding 1: Post-WWII globalization succeeded before it strained.

The U.S.-led globalization order produced reconstruction, trade expansion, security coordination, financial liquidity, technological diffusion, and institutional continuity. Its weakness was not immediate failure, but cumulative imbalance: debt, financialization, offshoring, unequal gains, strategic dependence, and domestic distrust.

Finding 2: Trump is not the root cause.

The forces behind Trump—China’s rise, the 2008 crisis, deindustrialization, war fatigue, border politics, asset inequality, and institutional distrust—preceded him. His presidency gives those pressures political and administrative form.

Finding 3: Multipolarity is not American collapse.

The United States remains powerful. The dollar remains dominant. U.S. alliances remain valuable. U.S. technology remains central. Multipolarity means the end of uncontested system management, not the end of American power.

Finding 4: China policy is the central test case.

The United States can no longer treat China as a manufacturing extension of the dollar-led order. China is a rival pole whose industrial, technological, military, financial, and diplomatic power changes the logic of globalization.

Finding 5: Economic security is now national security.

Semiconductors, rare earths, pharmaceuticals, energy, food systems, ports, shipping, telecommunications, data, and defense inputs are strategic infrastructure.

Finding 6: Dollar dominance remains strong but contested.

The dollar’s continued majority share of global reserves confirms that it remains dominant, while its decline from early-2000s levels and the growth of diversification confirm that monetary power is no longer uncontested.

Finding 7: Multipolarity is not automatically liberating.

A multipolar world may reduce dependence on Washington, but it may also produce rival control systems: regional payment blocs, digital currencies, sanctions networks, programmable access, financial surveillance, and intensified state-corporate coordination.

Finding 8: Domestic legitimacy is decisive.

No global strategy can survive if citizens experience the system as extraction, decline, or betrayal. The legitimacy of U.S. power abroad depends on the credibility of the economic order at home.

XIII. Strategic Risks

The first risk is trade escalation without productive reconstruction. Tariffs can create leverage, but if they are not paired with industrial strategy, they can raise costs while leaving dependency intact.

The second risk is financial instability. The world remains deeply dollar-dependent. A disorderly erosion of dollar primacy would not simply weaken the United States; it could destabilize debt markets, trade finance, reserve management, and global liquidity.

The third risk is bloc hardening. IMF research on geoeconomic fragmentation warns that fragmentation can reduce diversification benefits as countries restrict economic relationships to geopolitical allies.

The fourth risk is alliance distrust. Burden-sharing is necessary, but public coercion can weaken trust. The challenge is to reprice alliances without destroying the cohesion that gives them strategic value.

The fifth risk is authoritarian drift. Emergency economics, digital money, sanctions compliance, industrial policy, surveillance infrastructure, and public-private governance can centralize power. These tools may be justified by real threats, but without legal safeguards they can weaken privacy, due process, market autonomy, and democratic accountability.

The sixth risk is domestic fracture. If the costs of transition fall again on workers and communities while asset owners and politically connected institutions are protected, the legitimacy crisis will deepen.

The seventh risk is strategic overcorrection. The old globalization model failed to protect national resilience. But overcorrection could produce autarkic fantasy, indiscriminate protectionism, alliance rupture, and unnecessary confrontation.

The central risk is not transition itself. The central risk is unmanaged transition.

XIV. Strategic Requirements

1. Integrate national power.

Problem: U.S. policy is still too often fragmented across trade, defense, finance, energy, immigration, technology, and domestic policy.

Requirement: Treat these domains as one strategic system. Tariffs without industrial policy are incomplete. Industrial policy without energy security is fragile. Dollar primacy without fiscal credibility is vulnerable. Defense strategy without manufacturing capacity is hollow.

Operational implication: Establish a national economic-security framework that links trade enforcement, defense-industrial planning, energy permitting, critical-mineral strategy, port capacity, workforce development, and fiscal discipline.

2. Rebuild strategic production.

Problem: Dependence on rival or fragile supply chains creates coercive vulnerability.

Requirement: Prioritize selective resilience in semiconductors, defense inputs, critical minerals, energy systems, pharmaceuticals, food systems, ports, shipping, telecommunications, machine tools, and advanced manufacturing.

Operational implication: Use targeted procurement, permitting reform, workforce pipelines, allied co-production, tax incentives, and performance-based industrial support. The objective is not autarky. It is the ability to withstand coercion, war, sanctions, pandemics, or supply disruption.

3. Compete with China through institutional strength.

Problem: Tariffs alone cannot solve a structural industrial and technological rivalry.

Requirement: Pair trade pressure with industrial depth, allied coordination, technology leadership, investment screening, export controls, supply-chain diversification, and domestic renewal.

Operational implication: Treat China policy as a whole-of-system strategy, not merely a tariff schedule. The United States should coordinate with allies on semiconductors, critical minerals, maritime security, AI standards, telecommunications, research security, and investment screening.

4. Reprice alliances without breaking them.

Problem: The United States needs allies to carry more burden, but alliance distrust can weaken U.S. power.

Requirement: Increase allied contributions to defense, industrial resilience, energy security, technology protection, and supply-chain security while preserving U.S. strategic benefits.

Operational implication: Use NATO’s 5 percent commitment as a benchmark for capability planning, defense production, infrastructure resilience, and regional responsibility—not merely as a spending slogan.

5. Defend dollar credibility through discipline.

Problem: Dollar dominance can erode at the margins even without collapse.

Requirement: Preserve fiscal seriousness, institutional trust, productive capacity, liquid markets, rule of law, and restrained use of sanctions.

Operational implication: Treat debt sustainability, Treasury-market resilience, sanctions restraint, and industrial capacity as linked pillars of monetary power. Dollar primacy is not only a financial asset; it is a strategic system.

6. Treat energy and real assets as foundations of sovereignty.

Problem: Financial claims cannot substitute for control over essential material systems.

Requirement: Treat energy, land, water, food, logistics, housing, minerals, grid infrastructure, ports, and industrial capacity as the physical base of national power.

Operational implication: Link energy policy to industrial strategy, defense production, grid reliability, critical-mineral access, and household affordability. Energy abundance without infrastructure is insufficient; energy transition without reliability is strategically dangerous.

7. Put constitutional limits around digital finance.

Problem: Digital money, payment systems, identity frameworks, sanctions compliance, and emergency financial tools can create conditional-access infrastructure.

Requirement: Govern these systems transparently, with due process, privacy protections, legislative oversight, and clear limits on emergency authority.

Operational implication: Any modernization of payments, digital identity, CBDC-like infrastructure, stablecoin regulation, or sanctions compliance should include explicit protections against political exclusion, warrantless financial surveillance, and indefinite emergency powers.

8. Restore the domestic bargain.

Problem: A foreign-policy strategy cannot survive a legitimacy crisis at home.

Requirement: Reconnect national strategy to rising real wages, affordable housing, credible borders, regional investment, institutional accountability, fiscal discipline, and visible national renewal.

Operational implication: Measure success not only by GDP, equity markets, or trade statistics, but by whether strategic policy improves household security, regional opportunity, productive employment, and public trust.

XV. Final Strategic Assessment

Trump’s current presidency is not merely a continuation of his first term. It is the live implementation phase of a larger systemic adjustment. The first term revealed the instability of post–World War II globalization; the current term is testing whether the United States can convert that disruption into a disciplined strategy for multipolar competition.

Success will depend less on rhetorical confrontation than on execution: rebuilding productive capacity, preserving dollar credibility, strengthening alliances without hollowing them out, managing China competition without strategic overreach, limiting digital control systems, and restoring domestic legitimacy.

His critics are right that his methods can damage trust, raise uncertainty, increase costs, and substitute confrontation for institutional discipline. His supporters are right that he identified failures many elites minimized: China dependence, industrial decline, alliance underpayment, border disorder, financialized inequality, and the political costs of unrestricted globalization.

The strongest interpretation is structural. Trump is a volatile transitional figure. His first term exposed the end of uncontested American system management. His current presidency is testing whether that exposure can become durable strategy.

The future of American power will not be determined by whether the old globalization model can be restored. It will be determined by whether its successor can be built without systemic rupture: productive enough to restore domestic confidence, disciplined enough to preserve monetary credibility, strong enough to compete with China, restrained enough to avoid authoritarian drift, and constitutional enough to retain the legitimacy that post–World War II globalization ultimately lost.

Main Paper

Executive Thesis

Donald Trump’s presidency should be understood as a two-phase stress event in the crisis of post–World War II globalization. The system under analysis is not “globalization” in the abstract, but the specific U.S.-led model that combined Bretton Woods monetary institutions, Cold War security guarantees, post-1971 fiat-dollar finance, post-Cold War unipolarity, WTO-era trade liberalization, China-integrated supply chains, and financialized asset growth.

That model succeeded for decades because it allowed the United States to act simultaneously as reserve-currency issuer, security guarantor, consumer market, liquidity provider, institutional sponsor, and manager of allied capitalism. But its late-stage form produced contradictions that could no longer be contained inside the post-Cold War consensus: dollar dominance required expanding debt; open trade accelerated industrial hollowing; China integration created a peer competitor; alliance leadership encouraged burden imbalance; efficient supply chains created strategic dependence; financialized growth widened the gap between asset owners and wage earners; and border politics exposed declining confidence in state capacity.

Trump did not create these contradictions. His first term forced them into open political conflict. His tariffs, China confrontation, NATO pressure, immigration policy, energy posture, and “America First” framework challenged the operating assumptions of late-stage post-WWII globalization: that free trade automatically served U.S. interests; that China would liberalize through integration; that allies could rely indefinitely on U.S. security guarantees without greater burden-sharing; that supply chains could be optimized for cost without regard to sovereignty; and that financial strength could substitute for industrial depth.

His current presidency is testing whether that rupture can be converted into a coherent governing doctrine for multipolar competition. Trade policy, China strategy, alliance burden-sharing, energy security, border control, industrial policy, digital finance, and dollar credibility are no longer separate policy domains. They are linked theaters in the attempted renegotiation of the post-WWII globalization model.

The central question is therefore not whether Trump personally designed the transition to multipolarity. He did not. The central question is whether the United States can move from late-stage, dollar-centered, finance-heavy, China-dependent globalization toward a more resilient, productive, and constitutionally accountable economic-security order without triggering trade escalation, alliance fracture, monetary instability, authoritarian drift, or domestic breakdown.

Core judgment: Trump is not the architect of multipolarity; he is the political instrument through which the United States is now testing whether the post-WWII globalization model can be renegotiated before it fails disorderly.

Key claim: Trump’s current presidency should be understood as the live implementation phase of a broader systemic adjustment: the attempt to move from late-stage post–World War II globalization toward a managed multipolar economic-security order.

Evidence base: Bretton Woods history, Federal Reserve dollar research, USTR trade-policy documents, NATO burden-sharing materials, IMF geoeconomic-fragmentation analysis, CBO fiscal projections, national-security documents, and institutional research on industrial policy, supply chains, and digital finance.

Transition: To evaluate this thesis rigorously, the paper must first define its scope, method, evidentiary standards, and the distinction between documented policy actions, structural forces, interpretive frameworks, and speculative claims.

I. Purpose, Scope, and Method

This paper examines Donald Trump’s presidency as a diagnostic lens for the crisis of post–World War II globalization. The object of analysis is not Trump as a personality, nor Trumpism as a campaign style, nor populism as a standalone phenomenon. The object of analysis is the U.S.-led globalization model that emerged after 1945 and evolved through Bretton Woods monetary institutions, Cold War security guarantees, post-1971 fiat-dollar finance, post-Cold War unipolarity, WTO-era trade liberalization, China-integrated supply chains, and financialized asset growth.

The paper’s central question is:

How does Trump’s presidency reveal the structural crisis of post–World War II globalization, and can the current presidency convert first-term rupture into a coherent doctrine for multipolar competition?

This question reframes Trump from sole cause to stress event. Trump did not create the crisis of post-WWII globalization, but his presidency gives that crisis unusually visible political and administrative form. His first term forced latent contradictions into open conflict. His current presidency is testing whether those disruptions can be institutionalized into a governing framework for trade, China competition, alliance burden-sharing, industrial policy, energy security, border enforcement, monetary credibility, digital finance, and domestic legitimacy.

The paper is therefore structural rather than biographical. It does not attempt to explain Trump’s psychology, campaign persona, media strategy, or electoral coalition except where those factors illuminate the larger systemic transition. Nor does it attempt to provide a general history of globalization. Its purpose is narrower: to analyze how the late-stage U.S.-led globalization model is being contested, renegotiated, and partially restructured through Trump-era policy.

The paper proceeds from a specific definition of post–World War II globalization: a layered system of U.S. monetary leadership, alliance guarantees, open-market access, institutional management, financial liberalization, and globally integrated production. This system produced reconstruction, trade growth, technological diffusion, financial liquidity, allied stability, and American influence. It also generated mounting contradictions: dollar privilege alongside debt saturation; open trade alongside industrial erosion; China integration alongside strategic rivalry; alliance leadership alongside burden fatigue; supply-chain efficiency alongside national-security exposure; financialized growth alongside household insecurity; and labor mobility alongside border-politics backlash.

The methodological approach is organized around four categories of evidence and interpretation.

First, the paper examines documented policy actions. These include tariff measures, USTR actions, trade-policy reviews, China policy, national-security documents, NATO burden-sharing pressure, border enforcement, energy policy, industrial-policy measures, digital-finance debates, and current efforts to link trade, production, and security.

Second, the paper analyzes structural economic and geopolitical forces. These include reserve-currency burdens, federal debt expansion, industrial offshoring, trade imbalances, supply-chain fragility, China’s rise, Russia’s reassertion, alliance overstretch, migration pressure, energy insecurity, financialization, technological rivalry, and declining domestic trust in elite-managed globalization.

Third, the paper evaluates interpretive frameworks. These include structural-realist arguments about great-power competition, political-economy arguments about financialization and industrial decline, and Catherine Austin Fitts-style arguments about financial centralization, digital money, asset control, public-private governance, and surveillance-capable payment systems. These frameworks are used to generate analytical questions, not to substitute for evidence.

Fourth, the paper separates speculative or contested claims from documented fact. Claims about hidden intent, covert coordination, deliberate system design, or unified elite planning require a higher evidentiary threshold than claims about public policy, official documents, institutional behavior, market structure, or measurable economic trends. Where a claim is interpretive, the paper identifies it as interpretive. Where evidence is incomplete, the paper treats the conclusion as provisional.

This evidentiary discipline is essential because the subject is vulnerable to two opposite errors. The first is partisan reduction: treating Trump as either the sole villain who damaged an otherwise stable order or the sole visionary who saw what elites could not. The second is conspiratorial compression: treating complex institutional adaptation as proof of a single hidden design. This paper rejects both errors. It treats Trump as a volatile transitional figure operating inside a system whose contradictions were already advanced before his presidency and have become more acute during his current term.

The causal structure of the paper is straightforward. Post-WWII globalization created stability and growth while embedding dependencies around the dollar, U.S. security guarantees, offshored production, and global supply chains. The post-Cold War expansion of that model intensified the contradictions through China integration, financialization, debt expansion, industrial offshoring, and regional inequality. These contradictions weakened domestic legitimacy and strategic resilience. Trump’s first term converted latent structural pressure into open political rupture. His current presidency is testing whether rupture can become doctrine.

The paper’s argument is therefore neither nostalgic nor accelerationist. It does not assume that the old order can be restored in its prior form. Nor does it assume that disruption, tariffs, fragmentation, or multipolarity are inherently beneficial. The central issue is governance: whether the United States can move from late-stage postwar globalization toward a more resilient economic-security order without destroying the stabilizing advantages of the system it is attempting to revise.

The paper’s scope is limited in three ways. It does not present a complete economic history of the twentieth and twenty-first centuries. It does not evaluate every Trump policy. It does not attempt to predict the final structure of the emerging multipolar order. Instead, it assesses the strategic transition now underway and identifies the conditions under which that transition may become disciplined rather than disorderly.

The central working claim is that Trump is neither the origin of the crisis nor external to it. He is the political mechanism through which the United States is actively renegotiating the post-WWII globalization model it once managed. Whether that renegotiation succeeds depends less on the force of disruption than on the quality of execution: productive capacity, monetary discipline, alliance management, constitutional restraint, energy security, border credibility, and domestic renewal.

II. The Post–World War II Globalization Order: Architecture and Assumptions

A. The System Under Analysis

The post–World War II globalization order was not simply a collection of trade agreements, monetary rules, or diplomatic institutions. It was a layered U.S.-led architecture of monetary power, security guarantees, open-market access, institutional management, financial expansion, and globally integrated production. Its central premise was that American monetary credibility, military reach, institutional leadership, and consumer-market depth could organize first the non-communist world after 1945 and later the broader global economy after the Cold War.

This system should be distinguished from globalization in the generic sense. Cross-border trade, migration, finance, conquest, and technological exchange long predate the twentieth century. The subject here is narrower and more historically specific: the modern U.S.-centered globalization model that emerged after World War II, expanded through Cold War alliance structures, transformed after the 1971 end of dollar-gold convertibility, and reached its mature form during the post-Cold War unipolar era. By the early twenty-first century, this model combined dollar centrality, U.S. security guarantees, WTO-era trade liberalization, China-integrated supply chains, global capital mobility, financialized asset growth, and the assumption that market integration would reinforce a U.S.-led rules-based order.

B. Bretton Woods and Dollar Centrality

The first layer of this architecture was monetary. The Bretton Woods system placed the United States at the center of postwar economic reconstruction. The dollar became the anchor of international monetary stability, while the International Monetary Fund and World Bank became core institutions of postwar economic management. This arrangement reflected American material power at the end of World War II: unmatched industrial capacity, large gold reserves, military reach, and political legitimacy among allied states.

The Bretton Woods framework was not merely technical. It embedded the idea that U.S. monetary credibility could serve as a stabilizing foundation for international economic order. The dollar’s role as anchor currency created a system in which American domestic monetary choices had global consequences. From the beginning, then, postwar globalization rested on a dual premise: the United States would pursue national prosperity while also supplying the monetary foundation of the wider system.

C. Security-Backed Globalization

The second layer was security. The United States did not simply supply a currency and a market; it supplied protection. NATO, U.S. alliances in Asia, naval power, nuclear deterrence, and forward-deployed military capacity created the security environment within which allied economies could rebuild and integrate.

In this sense, post–World War II globalization was always security-backed globalization. The openness of markets, the convertibility of currencies, the stability of trade routes, and the confidence of investors were inseparable from American military and diplomatic commitments. The U.S. security umbrella lowered risk for allies, constrained adversaries, and enabled economic integration under American sponsorship.

This security architecture also shaped the political economy of allied states. Many allies could prioritize domestic reconstruction, welfare-state development, export competitiveness, and industrial planning while relying on the United States to provide the broader strategic environment. That arrangement strengthened American influence, but it also created the long-term burden-sharing problem that later became central to Trump-era alliance politics.

D. Institutional Governance

The third layer was institutional. The IMF, World Bank, GATT, and later the WTO provided rules, lending mechanisms, dispute processes, development finance, and trade-liberalization frameworks. These institutions did not eliminate national interest or geopolitical conflict, but they gave postwar globalization a legal and administrative structure.

Institutional governance allowed the United States to convert power into rules. The United States did not have to govern the system solely through direct coercion; it could govern through standards, market access, financial influence, voting power, dispute procedures, and alliance coordination. Institutions gave American leadership durability by embedding it in procedures that appeared more neutral than direct power politics.

This institutional layer also encouraged the belief that economic integration could moderate conflict. The governing assumption was that participation in shared institutions would make states more predictable, more market-oriented, and more compatible with U.S.-led norms. That assumption became especially important after the Cold War, when policymakers increasingly treated global economic integration as a mechanism of political convergence.

E. The Post-1971 Fiat-Dollar System

The fourth layer was the post-1971 fiat-dollar system. When formal dollar-gold convertibility ended, the dollar did not lose its global role. Instead, the system became more dependent on U.S. Treasury markets, dollar-denominated credit, global banking networks, central-bank coordination, and confidence in American financial institutions.

This shift made the system more flexible and expansive. It allowed the United States to run larger deficits, supply global liquidity, and support deeper capital markets. But it also increased the role of debt, asset prices, leverage, and financial engineering in the operation of global power. The post-1971 system made dollar primacy less metallic and more financial.

The long-term consequence was a deeper fusion of American power with global finance. Dollar dominance became less dependent on gold convertibility and more dependent on liquidity, institutional trust, Treasury-market depth, sanctions capacity, banking networks, and global demand for dollar assets. This gave the United States extraordinary advantages, but it also made the system more vulnerable to debt saturation, asset inflation, and financial instability.

F. Post-Cold War Unipolar Globalization

The fifth layer was post-Cold War unipolar globalization. After the Soviet collapse, the United States appeared to stand at the center of a largely uncontested international order. The central assumption of this period was that market liberalization, trade expansion, financial openness, and institutional integration would gradually align major economies with the preferences of the U.S.-led system.

The “Washington Consensus,” WTO expansion, capital mobility, privatization, deregulation, global supply chains, and technology integration all reflected this confidence. The system no longer merely organized the capitalist bloc against the Soviet Union; it aspired to become the default operating structure of the world economy.

This period produced the strongest belief that globalization and American leadership were mutually reinforcing. U.S. firms could organize global production, U.S. consumers could absorb imports, U.S. financial markets could recycle capital, U.S. institutions could set rules, and U.S. military power could stabilize the background conditions of exchange. The model appeared self-reinforcing. Its vulnerabilities were less visible because American power remained overwhelming.

G. China-Integrated Supply-Chain Capitalism

The sixth layer was China-integrated supply-chain capitalism. China’s integration into global markets, especially after its WTO accession, became one of the defining features of late-stage post–World War II globalization. Western capital, Chinese labor, global logistics, dollar finance, multinational corporate strategy, and technology transfer combined to produce an extraordinarily efficient manufacturing model.

This model lowered consumer costs, expanded corporate margins, and deepened global interdependence. But it also shifted industrial capacity, supply-chain leverage, and technological learning toward a state that did not become politically liberal, strategically subordinate, or fully compatible with U.S.-led rules.

This was one of the decisive contradictions of the late-stage model. China was integrated into the system as a production platform and growth market, but over time it became a rival industrial, technological, and geopolitical pole. The assumption that integration would produce convergence proved increasingly difficult to sustain. What had been treated as a commercial opportunity became a strategic dependency.

H. Financialized Asset Growth

The seventh layer was financialized asset growth. As production globalized and the dollar system deepened, American economic strength became increasingly tied to asset markets, equity valuations, real estate, corporate financial engineering, credit expansion, and central-bank liquidity.

This supported household wealth for asset owners, pension funds, institutional investors, and globally positioned corporations. But it also widened the gap between financial prosperity and productive security. Regions dependent on manufacturing, wage labor, affordable housing, and local investment often experienced the system not as global opportunity but as dislocation, precarity, and institutional abandonment.

Financialized growth created a political-economy problem that became increasingly difficult to manage. The system could generate rising asset values while many households faced stagnant wages, insecure employment, unaffordable housing, medical debt, student debt, and declining confidence in national institutions. In that environment, headline growth did not necessarily translate into legitimacy.

I. Assumptions Behind the Model

The assumptions behind this architecture were powerful. The first assumption was that American economic strength could support global monetary leadership. The second was that allies would accept U.S. leadership because it delivered security and prosperity. The third was that trade liberalization would produce broad gains and that adjustment costs could be managed domestically.

The fourth assumption was that China’s integration would encourage convergence rather than strategic rivalry. The fifth was that financial markets could allocate capital efficiently across borders. The sixth was that global supply chains could be optimized for cost without creating unacceptable security exposure. The seventh was that American domestic consent could survive the distributional effects of globalization.

For decades, many of these assumptions appeared plausible. The postwar order helped rebuild Europe and Japan, stabilized allied regions, supported trade expansion, reduced some consumer costs, encouraged technological diffusion, and amplified American influence. It provided the institutional and financial architecture through which the United States could transform national power into system management.

J. Built-In Contradictions

The problem was not that the system failed immediately. The problem was that its successes generated dependencies and imbalances that became harder to manage over time. Dollar dominance created enormous advantages, but also tied American power to debt expansion, global demand for U.S. financial assets, and confidence in Treasury markets. Security guarantees amplified U.S. influence, but also encouraged allied dependence and burden imbalance. Trade liberalization lowered prices and increased corporate efficiency, but contributed to industrial offshoring and regional decline.

China integration expanded global production, but produced a peer competitor with growing industrial, technological, and military capacity. Financialization created wealth for asset holders, but weakened the link between national prosperity and productive labor. Supply-chain optimization reduced costs, but increased exposure to coercion, disruption, and geopolitical shock.

These contradictions were not accidental deviations from the model. They were embedded in its structure. A reserve-currency issuer must provide liquidity to the world, often through deep and expanding debt markets. A security guarantor must bear costs that allies may underpay. A consumer-market hegemon may absorb imports in ways that weaken domestic production. A financialized system may reward capital mobility more than place-based investment. An efficiency-centered supply-chain model may minimize costs while maximizing strategic exposure.

K. Why This Architecture Matters for Trump’s Presidency

This architecture is essential for understanding Trump’s presidency. Trump did not enter a stable system and destabilize it from nowhere. He entered a system whose core assumptions were already under pressure. His trade policy challenged the assumption that openness automatically served U.S. interests. His China policy challenged the assumption that integration would produce convergence. His NATO pressure challenged the assumption that alliance leadership could remain underpriced. His border policy challenged the assumption that labor mobility and state legitimacy could be treated separately. His energy policy challenged the assumption that production and material capacity were secondary to financial and regulatory management. His industrial rhetoric challenged the assumption that financial strength could substitute for productive depth.

A serious account must therefore avoid two errors. The first is nostalgia: treating post–World War II globalization as a stable order disrupted only by Trump’s temperament. The second is rejectionism: treating the entire system as a failure because its late-stage contradictions became severe. The more accurate conclusion is that the system succeeded historically, then strained structurally. Its achievements were real, but its mature form became increasingly unable to reconcile external leadership with domestic legitimacy, financial dominance with productive capacity, and global integration with strategic autonomy.

The central assumption now being tested is whether the United States can remain the leading power in a system whose original foundations have changed. It no longer possesses the same uncontested industrial dominance it held after 1945. It no longer operates in the unipolar optimism of the 1990s. It no longer faces a China that can plausibly be treated as a subordinate manufacturing platform. It no longer enjoys unlimited domestic tolerance for trade deficits, industrial erosion, alliance asymmetry, financialization, or border disorder.

The post–World War II globalization order has not disappeared, but it no longer commands the same strategic or political legitimacy. The crisis of the model is therefore not simply geopolitical. It is monetary, industrial, social, institutional, and constitutional. It concerns whether a dollar-centered, security-backed, finance-heavy, China-integrated, supply-chain-dependent order can be renegotiated into a more resilient economic-security architecture.

III. The Erosion of the Post–World War II Globalization Model Before Trump

A. The System Was Already in Structural Erosion

The erosion of the post–World War II globalization model did not begin with Donald Trump. By the time Trump entered national office, the U.S.-led globalization order had already been weakened by China’s rise, Russia’s reassertion, the 2008 financial crisis, domestic deindustrialization, supply-chain fragility, fiscal pressure, border politics, and declining trust in elite-managed institutions. Trump’s significance lies not in creating these pressures, but in converting them into open political conflict.

This distinction is central to the paper’s argument. A weaker interpretation treats Trump as the origin of disruption: a political anomaly who destabilized an otherwise functioning order. A stronger interpretation recognizes that Trump emerged from a system already under strain. Late-stage post–World War II globalization had promised that open trade, financial integration, institutional management, and global supply chains would generate broad prosperity while reinforcing American leadership. By the 2010s, that promise had become increasingly difficult to defend. The model still produced wealth, efficiency, and geopolitical advantages, but it no longer commanded uncontested legitimacy.

The erosion of the model did not mean American collapse. The United States remained militarily powerful, financially central, technologically advanced, and institutionally influential. The dollar remained dominant. U.S. alliances remained valuable. American capital markets remained deep. The more precise claim is that the United States could no longer manage the global system on the same uncontested terms. The crisis was not the disappearance of American power; it was the weakening of American system management.

The system’s erosion occurred across three dimensions. Externally, rival powers challenged U.S.-led rules, institutions, and security arrangements. Economically, the globalization model produced dependencies that weakened industrial resilience and exposed strategic vulnerabilities. Domestically, the distributional effects of globalization weakened public trust in the institutions that managed the system. These three forms of erosion—geopolitical, economic, and domestic—converged before Trump.

B. China’s Rise and the Failure of Convergence

China’s rise was the most consequential structural challenge to late-stage post–World War II globalization. The dominant post-Cold War assumption was that integrating China into global markets would gradually make it more liberal, more cooperative, and more compatible with U.S.-led rules. Trade, investment, WTO accession, corporate integration, educational exchange, and institutional participation were expected to encourage convergence.

That expectation failed as a governing premise. China became a manufacturing superpower, a major exporter, a technological competitor, an infrastructure financier, and an increasingly assertive geopolitical actor. Its state-capitalist model preserved party-state direction over finance, land, industrial strategy, capital flows, technology policy, and strategic sectors. Rather than becoming a subordinate production platform inside a U.S.-led order, China became a rival pole of industrial, technological, diplomatic, and military power.

This was not merely a bilateral trade dispute. It was a contradiction inside the globalization model itself. The same system that allowed Western capital, Chinese labor, dollar finance, and global logistics to combine into an efficient production engine also strengthened a strategic competitor. What corporations experienced as cost efficiency, U.S. strategists increasingly experienced as dependency. What consumers experienced as lower prices, industrial regions often experienced as hollowing out. What policymakers once described as integration increasingly looked like strategic exposure.

The failure of convergence undermined one of the central assumptions of post-Cold War globalization: that market integration would align major powers with the U.S.-led system. China demonstrated that a state could benefit from global markets without becoming politically liberal, strategically subordinate, or fully governed by Western institutional norms. By the time Trump entered office, the engagement consensus was already intellectually vulnerable, even if it had not yet been fully abandoned as policy.

C. Russia’s Reassertion and the Limits of the Unipolar Moment

Russia’s reassertion exposed another weakness in the post-Cold War settlement. After the Soviet collapse, many Western policymakers assumed that Russia would remain weakened, peripheral, or gradually integrated into a U.S.-led order. That assumption underestimated Russia’s determination to preserve strategic autonomy, contest NATO expansion, use energy leverage, rebuild military capacity, and challenge Western influence in regions it considered vital.

Russia’s return as a disruptive geopolitical actor revealed that the unipolar moment was less settled than it appeared. The post-Cold War order had treated U.S. and allied institutional expansion as the natural extension of liberal internationalism. Russia increasingly interpreted that expansion as strategic encroachment. Whether one accepts or rejects Russia’s claims, the structural point remains: the post-Cold War system did not produce universal consent. It produced beneficiaries, dependents, challengers, and revisionist actors.

Russia’s reassertion also made clear that energy, military power, sanctions, and financial systems could not be separated. Energy exports, European dependence, banking access, sanctions exposure, defense spending, and alliance credibility became linked instruments of power. This foreshadowed one of the defining features of the emerging multipolar environment: economic relations would no longer remain insulated from security conflict.

The significance for this paper is that Russia’s reassertion helped reveal the limits of post-Cold War unipolarity before Trump. The U.S.-led order remained powerful, but it was no longer uncontested. Major states were beginning to resist, hedge against, or revise the system rather than simply adapt to it.

D. The 2008 Financial Crisis and the Loss of Stewardship Legitimacy

The 2008 financial crisis was a decisive blow to the legitimacy of Western financial stewardship. The post-1971 fiat-dollar system had made global finance more flexible and expansive, but also more dependent on leverage, asset prices, securitization, credit expansion, and central-bank crisis management. The crisis revealed that the system’s sophistication had created fragility.

The political consequences were profound. The institutions that had promoted financial liberalization, deregulation, global capital integration, and technocratic monetary management became associated with systemic failure. Governments and central banks intervened to stabilize banks, credit markets, and asset prices. These interventions may have prevented deeper collapse, but they also intensified the public perception that the system protected financial institutions more effectively than households, workers, and local communities.

The crisis did not end dollar dominance. In some respects, it reinforced the dollar’s safe-haven role. But it damaged the moral authority of the financialized globalization model. The public saw a system in which gains were privatized, losses were socialized, and asset markets were rescued while many households absorbed foreclosure, job loss, debt, and insecurity.

This mattered because post–World War II globalization depended not only on technical performance, but on legitimacy. If citizens believed the system generated broad prosperity, its burdens could be tolerated. If they believed it rewarded elites while exposing ordinary people to insecurity, its political foundation weakened. The 2008 crisis accelerated that legitimacy breakdown.

E. Domestic Deindustrialization and the Geography of Dislocation

The erosion of post–World War II globalization was also domestic. Large parts of the United States experienced globalization not as national renewal, but as industrial decline. Factory closures, wage pressure, regional inequality, loss of manufacturing capacity, declining local tax bases, family instability, addiction crises, and institutional distrust became central features of the political landscape.

These effects were uneven. Major metropolitan regions tied to finance, technology, higher education, government, and professional services often benefited from globalization. Asset owners benefited from rising equity and real-estate values. Multinational firms benefited from supply-chain optimization and global market access. But many industrial communities experienced the same system as disinvestment.

This uneven geography of globalization became politically explosive. The old policy answer was that free trade produced aggregate gains and that displaced workers could be helped through retraining, mobility, education, or adjustment assistance. In practice, many communities experienced adjustment not as transition but as abandonment. The loss was not only economic. It was civic, cultural, and institutional.

Trump’s political rise cannot be understood apart from this geography of dislocation. His critique of trade agreements, China, immigration, global elites, and industrial decline resonated because it gave political language to communities that had lost trust in the promises of globalization. Whether his remedies were sufficient is a separate question. The grievance itself preceded him.

F. Supply-Chain Fragility and Strategic Exposure

Late-stage post–World War II globalization optimized production for efficiency, not resilience. Firms built global supply chains around cost minimization, just-in-time inventory, regulatory arbitrage, labor-cost differentials, logistics efficiency, and scale. This model lowered prices and increased profitability, but it also created concentrated dependencies in critical sectors.

The problem was not always visible under stable conditions. In ordinary times, efficient supply chains looked like rational economic organization. Under stress, they became strategic vulnerabilities. Dependence on foreign production for semiconductors, pharmaceuticals, rare earths, medical supplies, telecommunications equipment, energy inputs, shipping capacity, and defense-related components created exposure to disruption, coercion, export controls, sanctions, war, pandemics, and political pressure.

This was a structural contradiction. The globalization model treated production location as a matter of efficiency. But in a world of strategic rivalry, production location becomes a matter of sovereignty. A state that depends on rivals or unstable regions for essential goods cannot fully separate commerce from security.

Trump’s trade and industrial rhetoric gained force because this vulnerability had already developed. He did not invent supply-chain dependence. He politicized it.

G. Fiscal Pressure, Dollar Burdens, and Financialization

The U.S.-led globalization model also faced pressure from the fiscal and monetary side. Dollar dominance gave the United States extraordinary advantages: deep capital markets, global demand for Treasury securities, lower borrowing costs, sanctions capacity, and the ability to supply liquidity during crises. But those advantages carried burdens.

A reserve-currency issuer must provide safe assets and liquidity to the world. Over time, that role became tied to federal debt expansion, Treasury-market depth, current-account imbalances, and the financialization of American economic power. The United States could consume more, borrow more, and import more because the rest of the world wanted dollar assets. But this also reinforced a model in which financial claims expanded faster than productive renewal.

Financialization did not simply enrich Wall Street. It reshaped the political economy of the country. Equity markets, housing values, retirement accounts, corporate debt, private equity, monetary policy, and asset-price stability became central to economic management. This created a dilemma: the United States needed to rebuild productive capacity, but its financial system depended heavily on asset values, liquidity, and debt expansion.

That dilemma existed before Trump. His presidency exposed it because he criticized globalization while also relying on asset-market performance as proof of economic strength. This contradiction was not merely personal. It reflected the structure of the system itself: a political revolt against globalization operating inside a financialized economy built by globalization.

H. Border Politics and the Crisis of State Capacity

Border politics also reflected the erosion of the globalization model. Immigration is often discussed as a cultural issue, but in the context of post–World War II globalization it also concerns labor markets, public finance, housing, law enforcement, sovereignty, and state capacity.

Late-stage globalization encouraged the movement of goods, capital, services, information, and labor. These flows produced benefits, but they also created political pressure when citizens believed the state had lost control over borders, wages, public services, or legal enforcement. Border politics became a proxy for a larger question: who bears the adjustment costs of globalization?

This does not mean immigration is inherently harmful. Lawful immigration can strengthen innovation, entrepreneurship, agriculture, health care, technology, demographics, and national dynamism. The stronger point is that immigration policy cannot be separated from labor-market strategy, housing capacity, employer enforcement, asylum administration, wage protection, and public trust.

Trump’s border politics became powerful because many citizens interpreted border disorder as evidence of institutional failure. Whether every perception was empirically accurate is less important than the structural meaning: a state that cannot credibly manage entry, labor flows, and legal enforcement loses legitimacy. That legitimacy problem was already visible before Trump.

I. Institutional Distrust and the Collapse of Consensus

By the time Trump rose politically, distrust of institutions had become one of the defining features of American public life. Political parties, media organizations, universities, financial institutions, intelligence agencies, international organizations, and corporate leadership all faced declining confidence from large parts of the public.

This distrust was not reducible to misinformation or polarization, though both played roles. It reflected accumulated experience: financial crisis, war fatigue, industrial decline, uneven globalization gains, border disputes, elite insulation, cultural fragmentation, and the perception that major decisions were made by institutions unaccountable to ordinary citizens.

The post-Cold War consensus had depended on elite confidence. Trade deals, financial liberalization, China engagement, alliance management, immigration policy, and technocratic governance were often justified by expert consensus. When trust in that consensus weakened, the political space opened for a figure willing to attack the entire framework.

Trump’s rise was therefore not an inexplicable deviation from political normalcy. It was evidence that the legitimacy structure supporting late-stage post–World War II globalization had weakened. His presidency did not merely disrupt consensus; it revealed that the consensus had already lost authority among a large share of the electorate.

J. Fragmentation as an Institutional Recognition of Crisis

The erosion of the model is now recognized even by institutions that helped manage globalization. Terms such as geoeconomic fragmentation, de-risking, friend-shoring, strategic autonomy, supply-chain resilience, and economic security have entered mainstream policy language. This matters because it shows that concerns once associated with populist critique have become institutional concerns.

Geoeconomic fragmentation refers to the increasing tendency of states to organize trade, finance, technology, investment, and supply chains around geopolitical alignment rather than pure efficiency. This does not mean globalization ends. It means globalization becomes more regionalized, securitized, and conditional.

The rise of fragmentation language confirms the central claim of this section: the model was already eroding before Trump. Trump made the erosion politically explicit, but he did not invent the underlying movement. The world was already shifting away from a model in which U.S.-led globalization could be treated as the natural, neutral, and uncontested framework for global economic life.

K. Why Pre-Trump Erosion Matters

The pre-Trump erosion of post–World War II globalization matters because it changes how the paper must interpret Trump’s presidency. If the system was stable before Trump, then Trump appears primarily as a disruptor. If the system was already eroding, then Trump appears as a volatile transitional figure operating inside a deeper structural crisis.

The second interpretation is stronger. Trump did not create China’s rise. He did not create the 2008 financial crisis. He did not create deindustrialization. He did not create the reserve-currency dilemma. He did not create allied burden imbalance. He did not create the dependence of American prosperity on asset markets. He did not create supply-chain fragility or institutional distrust. But his presidency gave these pressures a political vehicle.